Recent readings of the harmonized index of consumer prices (HICP) suggest a nontrivial risk of dipping into deflation in the euro area. While ECB's Draghi sticks to his "subdued price pressures" line, the IMF's Madame Lagarde has already called central bankers to arms to fight the "ogre" of deflation. This post argues that asset price inflation--in particular housing--is driving an overlooked wedge between the HICP and the cost of living, which ECB and commentators should take into account.

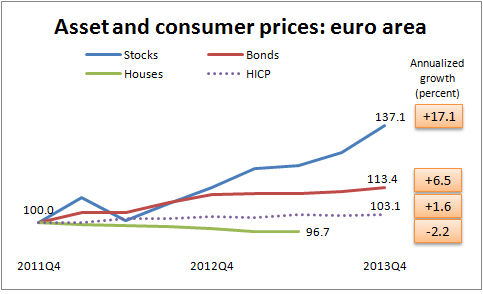

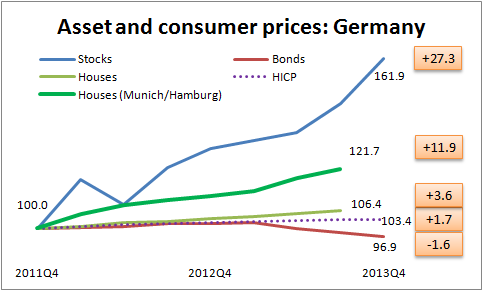

As shown below, asset prices have risen markably throughout Europe and Germany, much more than harmonized consumer prices. Stock and bond prices have advanced since 2011, albeit from depressed levels in some cases. Real estate prices are rising in Germany, among other euro area countries.

The HICP is largely aloof of asset price inflation. One perennially controversial item is the cost of housing. Currently, Eurostat's HIPC assigns small weight to housing--about 10 percent--as it excludes the implied cost of owner occupied housing given these are seen as capital expenditures. Eurostat is set to include owner-occupied housing cost in the HICP in a few years. This will significantly lift the weight of housing cost in the HICP, and lead to an increase in HICP measured inflation. Deflation no more.

House prices could and should also affect inflation expectation as the method for housing cost reflect average rather than marginal house prices. An example: Expectations of housing cost inflation of a young (and economics-literate) couple are less likely based on the constant rent they are currently paying for their current small student flat. Rather, the couple's expectations should be driven by run-away prices for family-size apartments in job-rich cities, such as Munich or Hamburg.

But there are more reasons for the ECB to take into account asset prices. Asset price inflation can stoke risks to financial stability. Juergen Stark once warned that "doing too much for too long" inhibits healthy balance sheet adjustments and leads to distortions. While financial stability is not at the core of ECB's mandate, ECB will increasingly become responsible for prudential and supervisory policies as well.

It is not deflation, it is the incapacitated transmission channels that ECB needs to fix. To achieve that, unconventional (and un-German) measures may be needed to avoid fueling unhealthy asset price inflation.